Master derivatives.

Price like a trader.

Black-Scholes pricers with greeks in 3D, the volatility smile under Heston and SABR, eight barrier variants, structured products and a four-module rates workbench. Plus 230+ market-tested interview questions to close the loop.

Free pricers, no account needed · Sign up only for Pro features · cancel anytime

Can you answer these?

A taste of the 230+ questions in the Coach. Real questions from FT / IB / hedge fund interviews — answers + rationales live inside, free with a quick sign-up.

230+ answered Q&A across 20 categories · printable cheat sheets · cancel anytime.

Delta = 0, Gamma = 1M EUR. Spot rises 5%. What is my new Delta?

Cash gamma of 1M means Delta moves by 1M per 1% of spot. A +5% move ⇒ +5M of Delta — you are now long 5M.

I hold an OTM call. Implied vol goes to 0. What is my Delta?

With zero vol the call can never finish in-the-money, so it is worthless and its Delta collapses to 0.

Short on time? Read every answer in one scroll.

No quiz, no scoring — just the 230+ interview questions with their answer right below each one. Pick a category, search by keyword, and revise fast the night before the interview.

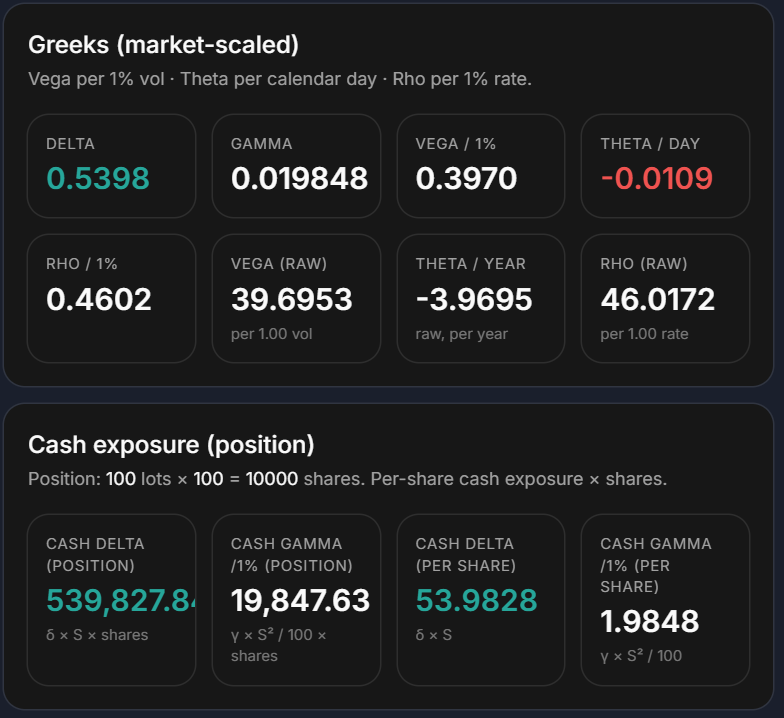

Market-scaled greeks, ready for the desk.

Vega per 1% vol, theta per calendar day, rho per 1% rate. Cash delta and cash gamma scaled by lot size and contract multiplier — same numbers a desk uses to hedge.

Built on the same Black-Scholes-Merton engine that drives the 3D surface above. Closed-form when possible, Fourier integration or binomial trees when it's not.

Everything you need to master derivatives

Built around pure-Python pricing engines with proper math — closed form when possible, Fourier integration or binomial trees when it's not.

Vanilla Options

Black-Scholes-Merton pricing with the six greeks, an interactive 3D surface, and a step-by-step formula breakdown.

OpenVolatility Models

Generate the IV smile parametrically — Heston via Fourier integration and SABR closed form, with skew + curvature metrics.

OpenBarrier Options

Eight Reiner-Rubinstein variants (Down/Up × In/Out × Call/Put). Greeks, in/out parity, knock probability, payoff chart.

OpenStructured Products

Turbo, Discount and Bonus certificates with the full replication breakdown and interactive 2D payoff charts.

OpenFixed Income

Four-module workbench — coupon bonds, IRS, callable bonds (short-rate tree) and convertibles (Tsiveriotis-Fernandes).

OpenxVA · CVA

Credit Valuation Adjustment for a vanilla IRS. 5-step pedagogical pipeline (forwards → exposure → PD → CVA), bilateral mode for DVA / bCVA, reference presets.

OpenInterview Coach

230+ market-tested derivatives questions across 20 categories. Scored exam mode and flash-card recto/verso mode.

Open